Wide of the Prize: Fintech and Retail Investment Platforms

New fintech and traditional retail investment platforms ignore glaring revenue and macro opportunities present in the industry. Efforts focus on selling picks—of varied price—to miners; instead, marketing gold and maps could be a more fruitful course.

New fintech and traditional retail investment platforms ignore glaring revenue and macro opportunities present in the industry. Efforts focus on selling picks—of varied price—to miners; instead, marketing gold and maps could be a more fruitful course.

Moves in recent years by startups to remove trading fees has brought about increased competition. The strategic aim of such is to build traction, but ultimately, it highlights the overriding nature of retail wealth management: A commodity service. Price wars may lead to more vanity metrics, but will revenue and customer value follow in tandem?

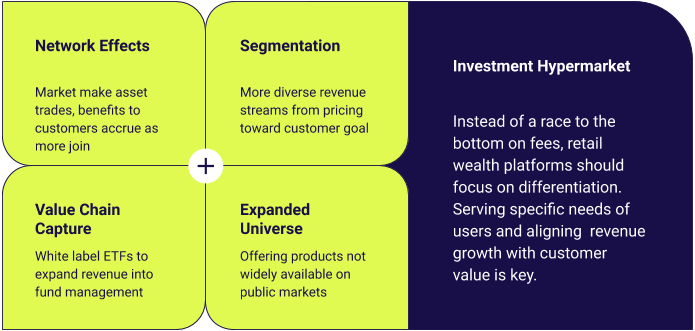

Some suggestions for wealth platforms to buck the trend to commoditisation are as follows:

- Build real network effects by market-making assets

- Equitable revenue strategies from segmenting customers better and marketing relevant services

- Using cost-efficient ETFs to market own-branded funds to move up into fund management value chains

- Readjusting to the new universe of investable assets and taking a “money portal” approach

How Retail Wealth Platforms Work

Retail wealth platforms refer to the broad industry of discount brokerages, stockbrokers and investment houses that serve personal savers’ investment needs, principally on a non-advised basis. Investors deposit funds, select investments and track portfolios through the suite of services offered. The internet helped the industry grow and more of the middle class to take proactive financial planning responsibility.

In terms of cost and revenue streams, retail wealth platforms make money through recurring and transactional streams, principally among the following:

Recurring:

- Custody charges on client assets under administration (“AUA”). Either flat or percentage-based

- Interest income on client cash balances

- Advisory fees for discretionary management services

- In-house fund management charges

Transactional:

- Trading fee commissions

- Stock lending fees (not deployed by all platforms)

- Order flow routing from selling liquidity to larger market makers

The best way to look at this visually is through an actual example from the UK. From Hargreaves Lansdown’s (“HL”) 2020 results, 73% of its revenue was recurring and 43% alone from custody charges on AUA.

Hargreaves Lansdown 2020 Revenue by Type

Substandard Business Models?

On the face of it, the retail wealth investing business model looks attractive. But several factors are present that are consumer-unfriendly and potentially perilous for the industry going forward.

1. Glutinous or Unscalable AUA Charges

Most traditional retail wealth platforms use charges on AUA as the mainstay of their income stream, as seen with HL, which uses a lucrative percentage fee on client fund balances. Such a strategy is advantageous for platforms, but suboptimal for consumers: Is holding funds in custody an actual marginal cost? Over a lifetime of investing fees eat away at potential returns; the differential of HL’s 0.45% fee on a dormant portfolio of £100,000 growing at 5% over 30 years would result in £52,249 forgone return.

On the other end of the scale, some providers use flat fees, like Interactive Investor, which are more client-friendly, but from the business perspective, create perverse incentives. The absolute number of clients served must increase along with other ancillary incomes, like trading commissions. The former is finite, while the latter is incongruous with responsible wealth management; clients shouldn’t be actively trading; sometimes, the best investors are the ones that aren’t even alive.

2. The Nature of the Industry Is Commoditised

Price is the only real differentiator between wealth platforms. The universe of investable assets is mostly available to all, and regulatory efforts to open up account transfers have eroded switching moats. There is little consumer benefit from a retail wealth platform growing unless cost savings are passed on (note: Vanguard does this, due to its unique ownership model).

Like current accounts at banks, the future seems unclear for the retail wealth platform industry, due to little differentiation between product offerings.

3. Discretionary Management Doesn’t Scale

Financial advisory is not a scalable business. High-net-worth individuals (“HNWIs”) at the upper end tend to create family offices, with dedicated staff serving a tailored mandate. Other savvy HNWIs use small boutiques or one-person shows, with needs attended to in a bespoke manner.

Financial advisory for the rest of us is an opaque business model, with dubious value-add for customers. Take St James’s Place—which holds 12% market share in the UK for advisory services—where over 72% of its funds underperform benchmarks.

Retail wealth managers have made moves into the discretionary space, but the outcome is neither scalable nor appealing. The result is usually a bloated and expensive fund-of-funds approach, or roboadvising, which I will come to later.

4. Disappearing Interest Income

In FY 2019, HL earned 0.74% of interest spread on dormant cash in client accounts. As interest rates have fallen since and will probably stay there, this business line will lose significance for wealth platforms.

5. Fintech Entrants Lowering Fees and Encouraging (Old) Bad Habits

Fintech entrants highlight trading fees as a sign of tired industry practices, serving to remove them entirely. Following the example of Robinhood, traditional players like Charles Schwab followed suit by offering fee-free trading in the US.

The result of no transaction fees will neither be user or business-friendly. Marketing will encourage more trading, usually at the wrong end of a trade where platforms sell order flow. As a tactic for getting users, free trading has worked, but what is the business’s end game? Speculative transaction income and recurring income from AUA charges repackaged into a “premium” account offering does not sound like industry innovation.

Roboadvising repackages traditional bad habits; its current incarnation appears to be the algorithmic trading lipstick on the pig of regular portfolio rebalancing. Fees are expensive (in the range of 0.5% to 0.95% at PensionBee), exclusive of underlying funds’ OCF charges. As with HL’s situation, for a service with seemingly negligible marginal costs, where is the marginal value to customers from charging such linear fees for roboadvising?

Two wealth platform business models seem to exist:

- Encourage AUA growth and gouge customers on custody fees.

- Encourage trading to generate transactional revenue.

Ultimately, what the industry needs is a model that benefits consumers and wealth managers together: How can both profit sustainably and equitably?

Glaring Opportunity: Retail Investing Is Changing

Growth of Household Wealth

Household financial assets on a USD/capita basis have grown considerably over the past 25 years, outstripping inflation and going against a prevailing fall in household savings ratios.

Growth of Developed Country Wealth Vs US Inflation and Average Savings Ratio: 1995-2016

The accrual of wealth is generally assumed to come from salaries, but over the period, median disposable income grew slower than the pace of wealth; increases in total financial wealth came from households accruing more from existing assets. The generation-long rise in house prices is one such factor behind this.

The power of compounding is evident when looking at the different quartiles of wealth. For example, in the UK over the past decade, household wealth has grown, albeit by varying degrees, ranging from 23.2% for the lowest quartile of earners to 45.2% for the top quartile (ONS).

People Save More by Investing

The rise of wealth corresponds with more households saving into financial assets, over (almost) risk-less cash accounts. For UK individuals’ total wealth, the proportion in private pensions grew from 34% to 42% over the previous decade.

Composition of UK Household Wealth: 2006-2018

The reason why pension wealth has increased can be down to several possibilities:

- As long-term investments, the expected return (over cash returns) is higher, hence wealth accrues faster.

- The S&P 500 returned 13.6% annualised over the previous decade, such returns attracting inflows.

- Falling interest rates since 2008 forced the hand of investors to allocate more to equities, of which a pension offers tax-based advantages.

Removing property and physical wealth (i.e. jewellery) and just looking at financial wealth, at the last count in spring 2018, there was £8.2 trillion of UK household savings (ONS) allocated among the following:

- Private Pensions: £6.1 trillion

- Financial Wealth: £2.1 trillion

- Cash ISAs: £257 billion

- Stocks & Shares ISAs: £354 billion

- Non-tax-wrapped cash and financial assets: £1.5 trillion

The introduction of tax-wrapped ISAs has been an instigator of the shift to investing in the UK. ISA wealth grew at a CAGR of 4.42% from 2000 to 2019, and Stocks & Shares ISA balances overtook their cash equivalent in 2013.

Growth of Tax-Wrapped Savings Schemes in the UK: 2000-2019

68% of 2019’s Stocks & Shares ISA balances sat in funds (e.g., OEICs and ETFs), showing that the UK investors tend to delegate to funds for picking winning horses.

Funds are similar beasts to retail wealth platforms; they charge fees on the assets they manage. A clue for the rest of the article: Funds are a glaring opportunity for the platform industry.

The Money of Demographics

Inheritance Landslide

The western baby boomer generation won a genetic lottery by coming of age during unprecedented periods of peace and wealth generation (both in markets and property). Being the last cohort to compound risk-free market wealth from final salary private-sector pensions significantly favoured boomers’ fortunes.

Over the next decades, as boomer wealth passes to benefactors, many scenarios will come to play. Firstly, inequality gaps will rise due to the concentration effect of fortunate parents bequeathing equally-blessed offspring. More central in this article’s context, behavioural elements of wealth management will start to come into play.

Existing wealth management relationships and investing preferences will not necessarily pass down through lineage. For current providers, this is a risk and opportunity, in terms of net gains and losses. Behaviourally, asset allocation styles will change. The 60/40 passive tracker of the elderly parent may not resonate with the child who is more accustomed to cryptocurrencies, crowdfunding and ethical investing.

Disappearing State and Defined Benefit Pensions

The decline of defined benefit (“DB”) pensions has placed more obligation onto individuals for managing retirement finances. In 1997, 34% of private-sector workers were DB members, which by 2016 had fallen to 9% (ONS). As more DB workers retire, this proportion will continue to fall; Shell became the last FTSE 100 company to close its DB scheme to new workers in 2012.

Fewer DBs has stoked anxiety over whether the state pension can survive unscathed past the boomer cohort’s longer expected lives. The UK state pension is already seen as the worst in the developed world for benefits relative to average earnings (29% vs 100.6% in the Netherlands). Through force of hand, or decisiveness, individuals have to become self-empowered to secure their financial futures.

The result of the shift towards defined contribution pensions ratchets up the pressure to invest more aggressively to beat inflation and keep up with the Joneses. The product will be more thought placed into investing plans, split between passive, active and alternative asset instruments.

Societal Change is Afoot

Innovation Encourages Investing

Retail investing once had barriers that limited growth and penetration among everyday people. Driven by the following:

- Information: Stale prices in newspapers and slow-moving news generally inhibited the volume and quality of data consumed. The advent of smartphones, social media and 247 media opened the kimono.

- Access: SIPPs and ISAs have driven attention and delayered investing complexity. Technology has also widened competition and lowered costs, as noted previously.

- Scale: Investor-friendly practices like fractional ownership, low-cost trackers and free regular investing are all gifts borne from retail platforms gaining scale.

Longer Lives

UK life expectancy at birth (ONS, Figure 1) for males and females has risen, respectively, from 70.8 and 76.8 in 1980-82 to 79.3 and 82.9 in 2016-18. In stark financial terms, this requires, for men at least, savings provisions for almost a whole decade of extra living.

It’s not inconceivable to imagine that those born now could reasonably expect to live to 100. While it is also logical to surmise that working lives will extend, many diligent savers do it aspirationally, with desires to retire early, which you can see in the rise of the FIRE movement.

Rise of Self Directed Investing

The rise of investing has corresponded with the popularity of self-directed DIY strategies. Eschewing the advised approach may be down to cost considerations, a weariness of outsourced underperformance, or desire to learn. Data from the FCA and Mintel showed that in the UK, advised transactions comprised 43% of retail investment sales in 2014, which fell to 27% by H1 2018.

Hard data is hard to come by, and there are varying degrees of ambiguity about what constitutes someone being a self-directed investor. Boring Money reported in 2019 that £260 billion of AUA attributed to “direct online investors”. 2020 was a flashpoint for retail investing, fueled by stock market volatility, boredom, fewer sports gambling opportunities and reduced conspicuous spending. Robinhood alone reported 3 million new account openings in the first four months of the year. Daily trading on retail platforms grew by over 200% during the year.

Online Brokerage Volumes from US Retail Investors: 2008-2020

Carpe Diem: How can Retail Platforms Change

When looking at retail wealth management, there are two fronts. The old guard, with steady business models, earn excess returns at the expense of customer benefit. The new guard fights the norms but encourages behaviour that may indirectly compromise customers to make revenue.

How the industry needs to evolve and thrive are in the following areas:

1. Create Real Network Effects

Social has a holy grail aura among retail platforms as a means to build network effects amongst users. The thesis being that users collaborate and share ideas on the platform, with the community effect adding intangible value. To date, several services offering community-sourced trading idea strategies have failed to take off, one of note is Quantopian, which closed in late 2020.

Money is a private matter for most investors, and following other investors’ decisions without consequence lacks agency, especially if they are talking up their book.

Network effects can otherwise be built up by platforms making markets for asset transactions, instead of using external brokers for dealing. Such a move is risky and requires a balance to build up equal sides of buyers and sellers. If pulled off, it would allow customer trades to be matched off on tighter spreads, providing platforms with a real incentive to build up user numbers and let the benefits (i.e. the network effects) reinforce the brand.

2. Embrace Customer Segmentation

Retail wealth platforms appear to position themselves to specific segments. Hargreaves Lansdown appeals to beginners or those valuing a clean UX. However, once customers become more experienced, the pricing acts as a push factor to leave, with little effort to bend and retain. A failure to revisit the paradigms of an existing revenue model is behind the stubbornness.

Instead, platforms should look at the whole ecosystem, ranging those who treat investing like paying a bill, to hardcore day traders.

Serving segmented needs will lead to more largess and diversity of revenue while addressing specific customer value needs. Here are some examples that encompass subscription, transactional and variable pricing areas.

Subscriptions: Useful Tools for DIY Investors

Self-directed investors are savvy to AUA and transaction charges. Perhaps from hubris of not wanting to be lumped into the “dumb money” bracket, but also because through cognisance of fees’ drag on compounded returns.

A blanket subscription price assuages concerns because relative cost diminishes with pot size and psychologically, fees typically charge through direct debit, not asset balances.

Traction and retention derive from product differentiation, offering more of the tools used in asset selection can drive this. The onus is on getting users to stay on the website and let their “power user” halo effect amplify social media and blogs to attract more novice investors.

Wealth platforms should view their offering like tabs on a browser. At the moment, they just have the portfolio overview tab. Better technical analysis tools, backtesting, alternative data points, integrations into spreadsheets and social listening can augment the suite offering.

Positioning services more as a “Bloomberg for retail” will increase retention, time on site, and customer value through the bundle pricing effect. The end effect being differentiation and higher revenue per user.

Transactional Fees: Advice-Based Marketplace Services

For investors not confident enough to take the lead on all their investing choices, a better suite of services for financial planning wouldn’t go amiss. Instead of linear in-house discretionary advice services, building out a marketplace to accredited financial planners is more scalable and trustworthy.

Investors could have options to pay for specific elements:

- Courses in financial management

- Curated lists of investments that are relevant to their situational requirements

- Ad-hoc services within the tax, inheritance, trust and accountancy realms

The marketplace element reduces potential conflicts in using in-house services while lowering operational complexity and cost.

Performance-Based Scalable Charges: Aligned Managed Investing

AUA pricing is fairest for both sides at the low AUA end of the market. However, for such investors who are more indifferent to their investment choices, wealth managers should reimagine the current options available:

- Roboadvising has high two-layered pricing, with little accountability.

- In-house managed fund-of-fund models have excessive fees and conflicts of interest.

Reimagining the roboadvising form, to combine elements of active investing and performance-related compensation (i.e. the private equity model) would be a differentiator, which rewards both sides if got right. Imagine if inexperienced investors are offered a managed fund option, with a small proportionate fee option and then a “carried interest” element paid to the manager for beating a benchmark?

3. Integration up the Value Chain

Wealth platforms must move into more steps of the retail investing supply chain.

Investment Trusts, ETFs and mutual funds have annual management charges based on assets under management. Wealth platforms do not earn any of this charge and in general, (2017 average of 0.75%) they are higher than custody AUA charges (0.45% at HL).

The glaring miss I see from retail wealth platforms is that they have not yet moved into this space. Vanguard is the most prominent example of a service that serves investors as a fund manager and custody platform.

Launching a traditional active mutual fund requires capabilities in the area. A manager requires research analysts, traders and salespeople to market the product. Alpha is not a given; for example, 67% of US active funds underperform their benchmark.

Hargreaves Lansdown is prominent in marketing its funds, but they are poor. All but two of its funds have underperformed, perhaps due to the high fees charged from a fund-of-funds model, or through stock picking conflicts of interest embedded in HL’s business model. Less than 25% of HL’s AUA is in their funds, so overall, it’s not a model demonstrating significant success.

Fintech wealth managers could take a more scalable approach to integrate into fund management. Instead of building out an in-house active asset manager, they could team up with an existing one in a co-brand manner. There would be mutual interests of a distribution angle for the fund manager and a differentiator for the platform.

A scalable approach is marketing own-brand ETFs. Such an option presents less potential conflicts and operational complexity by using technology-based decisions for allocating and rebalancing. ETFs have gained more attention in the fintech era for innovative approaches to thematic portfolio baskets. Firms like AKR Invest, Lyxor, WisdomTree and VanEck spring to mind, but most intriguing is HANetf, which offers white labelled products: Exactly the kind of bolt-on differentiator a platform could look to use.

4. Expanded Universe of Offered Products

Wealth manager platforms are seemingly homogenous. Stocks and funds are widely available, and the only differentiator is how quickly a platform can offer them all. Using cost to differentiate, such as negotiating reduced fund OCF charges is an option (popular at HL), but can be murky: Am I being marketed a winner or a cheap kickback?

Differentiation comes from widening the perspective; less corner shop, more investment hypermarket. Build a platform that serves as the base for financial decisions across banking, investing, mortgage, alternatives and physical asset products. Expanding horizontally into more esoteric offerings would enable platforms to capture more of the value chain and retain users within its ecosystem.

One such example of this concept could be a platform that buys, or partners with a crowdfunding site and gains accreditation for customers to invest in private startups under their ISA wrapper.

Race to the Top, Not the Bottom

Retail wealth platforms have built business models at the bottom end of the value chain. To thrive long-term, instead of divide and conquer among customer segmentation, requires a more expansive business strategy.

Platforms need to offer a more comprehensive suite of tools to users and expand up and across the wider investing value chain. Moving more into originating proprietary financial products with more investor-aligned interests will capture more revenue, not at the expense of customer value. Customers need to be segmented better from a branding perspective and served more with more fiduciary responsibility, over just being a cash cow.